Singlife Flexi Retirement Review

The complete Pros and Cons on Singlife Flexi Retirement

Singlife Flexi Retirement (previously known as Aviva MyRetirementChoice III) is a retirement plan and annuity policy that empowers you to retire at the age of your wish. Choose and plan for your retirement with plenty of income payout options to suit the retirement lifestyle of your dreams.

Reviewed by InterestGuru on 16/05/2023

Singlife Flexi Retirement product details

Singlife Flexi Retirement is featured for Guaranteed Payout benefits in our 4 Best High Income Retirement Plans in Singapore (2023 Edition)

Singlife Flexi Retirement is featured for High Retirement Income benefits in our 5 Best Insurance Plans for Retirement Income (2023 Edition)

Singlife Flexi Retirement Rating on InterestGuru.sg: [usr=4.25]

Singlife Flexi Retirement Popularity on InterestGuru.sg: [usr=4.5]

Read about: The Aviva MyRetirement series of retirement products

- Life policy – Annuity

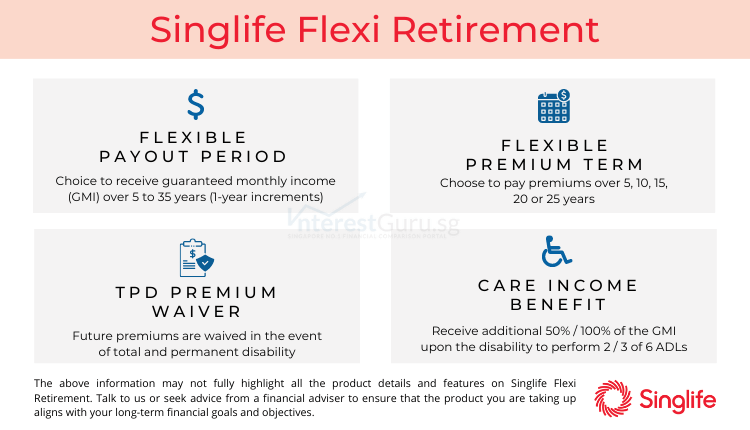

- Premium Term from 5, 10, 15, 20 or 25 years

- Flexible payout period anywhere from 5 to 35 years

- Various payout options; Guaranteed Monthly Income (GMI) + Potential Monthly Cash Bonus (MCB)

- You can choose to receive a lump-sum bonus upon reaching retirement age

- You can choose to convert the lump sum bonus into an additional monthly income

- Re-invest monthly retirement income at the prevailing non-guaranteed rates

- Care Income Benefit; receive every month

- An additional 50% of the GMI upon the disability to perform any

2 out of 6 ADL - An additional 100% of the GMI upon the disability to perform any

3 out of 6 ADL

- An additional 50% of the GMI upon the disability to perform any

- Fast Forward Option

- You can choose to receive the Care Income Benefit in a lump-sum

- Wide range of Premium waiver riders to waive premium for insurable events

- EasyTerm

- Payout of up to 5x the yearly premium in the event of Death, Terminal Illness, or Total and Permanent Disability

- Cancer Premium Waiver II

- Future premiums will be waived upon diagnosis of Major Cancer of insured

- Critical Illness Premium Waiver II

- Future premiums will be waived upon diagnosis of any of the covered critical illnesses of insured

- EasyPayer Premium Waiver

- All future premiums will be waived in the event of Death, Terminal Illness, or Total and Permanent Disability of the policyholder

- Payer Critical Illness Premium Waiver II

- Future premiums will be waived if the policyholder is diagnosed with any of the covered critical illnesses

- EasyTerm

- Enjoy hassle-free application with no medical check-ups

- 100% capital guaranteed at the time of retirement

Read about: Why your retirement planning starts now

Read about: Effects of compounding returns on your investments

Features of Singlife Flexi Retirement at a glance

Cash and Cash Withdrawal Benefits

- Cash value: Yes

- Cash withdrawal benefits: Yes

Health and Insurance Coverage

- Death: Yes

- Total Permanent Disability: Yes

- Terminal Illness: Yes

- Critical Illness: No

- Early Critical Illness: No

Health and Insurance Coverage Multiplier

- Death: No

- Total Permanent Disability: No

- Terminal Illness: No

- Critical Illness: No

- Early Critical Illness: No

Optional Add-on Riders

- EasyTerm

- Cancer Premium Waiver II

- Critical Illness Premium Waiver II

- EasyPayer Premium Waiver

- Payer Critical Illness Premium Waiver

Additional Features and Benefits

Yes.

For further information and details, refer to Singlife website. Alternatively, fill up the form below and let us advise accordingly.

Read about: How can I accumulate a million dollar (Realistically)

Read about: The Complete Guide to Retirement Planning (2023 Edition) *NEW*

Policy Illustration for Singlife Flexi Retirement, Paul

Paul, age 40, purchases Singlife Flexi Retirement as his retirement plan. He chooses to pay a yearly premium of S$18,579.50 for the next 10 years with a retirement age of 66.

At age 67, with a total of S$185,795 paid in premiums, Paul is entitled to a non-guaranteed lump sum bonus which he decides to convert into additional monthly income. Paul starts receiving a total projected monthly income of S$2,938.00 for the next 20 years.

By age 87, Paul has received a total projected income of S$705,120 from Singlife Flexi Retirement and the policy comes to an end.

Of the total projected income, S$240,000 is guaranteed, and S$465,120 is non-guaranteed.

Policy Illustration for Singlife Flexi Retirement, Tim

Tim, age 40, purchases Singlife Flexi Retirement as his retirement plan. He chooses to pay a yearly premium of S$8,302.05 for the next 25 years with a retirement age of 66.

At age 67, with a total of S$207,552 paid in premiums, Tim is entitled to a non-guaranteed lump sum bonus which he decides to convert into additional monthly income. Tim starts receiving a total projected monthly income of S$2,256.74 for the next 20 years.

By age 87, Tim will have received a total projected retirement income of S$541,618 from Singlife Flexi Retirement and the policy comes to an end.

Of the total projected income, S$240,000 is guaranteed, and S$301,618 is non-guaranteed.

Key Difference between Tim and Paul’s Singlife Flexi Retirement Journey

Both Paul and Tim started retirement planning at the same age and also chose the same age to start retirement. However, we can see that Paul is clearly the winner here in almost all aspects.

Paul paid lesser in premiums but received a significantly higher projected monthly income than Tim.

This is because Paul paid his premiums in a shorter period of time than Tim did. This allows for his funds to accumulate for a longer time thereby achieving a better yield.

In order to get the highest return on your capital, you can seek to pay for premiums in the shortest amount of time such as a single premium, or 5 to 10 years if possible. to achieve the best results out of your retirement annuity plans.

Singlife Flexi Retirement may be suitable if you are looking for

Singlife Flexi Retirement may potentially be a good fit if the following matters to you:

- Regular cash payout upon your desired retirement age

- High non-guaranteed bonuses in a retirement annuity policy

- Saving regularly over a period of time

- Insurance options without medical underwriting

- Do not need access to the funds until retirement

- To potentially generate higher financial returns compared to bank accounts

- Future premium waiver in the event you become totally and permanently disabled

Singlife Flexi Retirement may not be suitable if you are looking for

Singlife Flexi Retirement may potentially be a bad fit if the following matters to you:

- Health and Protection coverage

- High insurance coverage for Death or Terminal Illness

- High insurance coverage for Early Critical Illness, Critical Illness or Total Permanent Disability

- Lump-sum payout upon maturity

- A one-time premium commitment with no further cash commitment

- Potentially higher financial returns compared to a pure investment product.

- Insurance policy with a high surrender value in the early years of the policy.

Read about: Why should you choose a shorter premium term on your insurance policies

Further considerations on Singlife Flexi Retirement

- How is Singlife or Singlife Flexi Retirement investment returns based on historical performance?

- How does Singlife Flexi Retirement compare with retirement plans and annuity policies from other insurance companies?

- Can Singlife Flexi Retirement fulfill my financial, insurance, health, and protection needs?

The above information may not fully highlight all the product details and features on Singlife Flexi Retirement. Talk to us or seek advice from a financial adviser before making any decision about Singlife Flexi Retirement.

Always ensure your long-term financial goals and objectives are aligned with the financial product you are considering taking up.

Read about: 3 best Retirement plans and Annuity policies in Singapore (2023 Edition) *Updated*

Where can I compare the payout and benefits of retirement plans and annuity policies?

Your retirement plans are meant to supplement your lifestyle and expenses in your golden years. Ensure your retirement plans matches the financial goal and objective you wish to achieve when you decided to talk a step back in life.

It is too late to regret once you have made your financial commitment. Specific product features, benefits, and payout will differ more than you think across insurance companies.

And even worse, to know you can compare retirement plans and annuity policies here, 100% free of charge on the InterestGuru.sg platform.

Is Singlife Flexi Retirement suitable for me?

Contact InterestGuru using the form below. Our panel of licensed financial advisers will advise accordingly, based on your financial profile and protection needs.

All financial reviews and proposals provided are 100% free of charge. There will be no obligation to take up any proposed financial products or services in any way.

*For a limited time, get attractive incentives when you take up any products that is proposed by our team of financial planners.

We compare quotations head to head on all leading insurers in Singapore