NTUC Income TermLife Solitaire Review

The complete Pros and Cons on NTUC Income TermLife Solitaire

NTUC Income TermLife Solitaire product details

NTUC Income TermLife Solitaire is featured for Lifetime coverage in our 8 Best Term Life Insurance Plan in Singapore (2023 Edition)

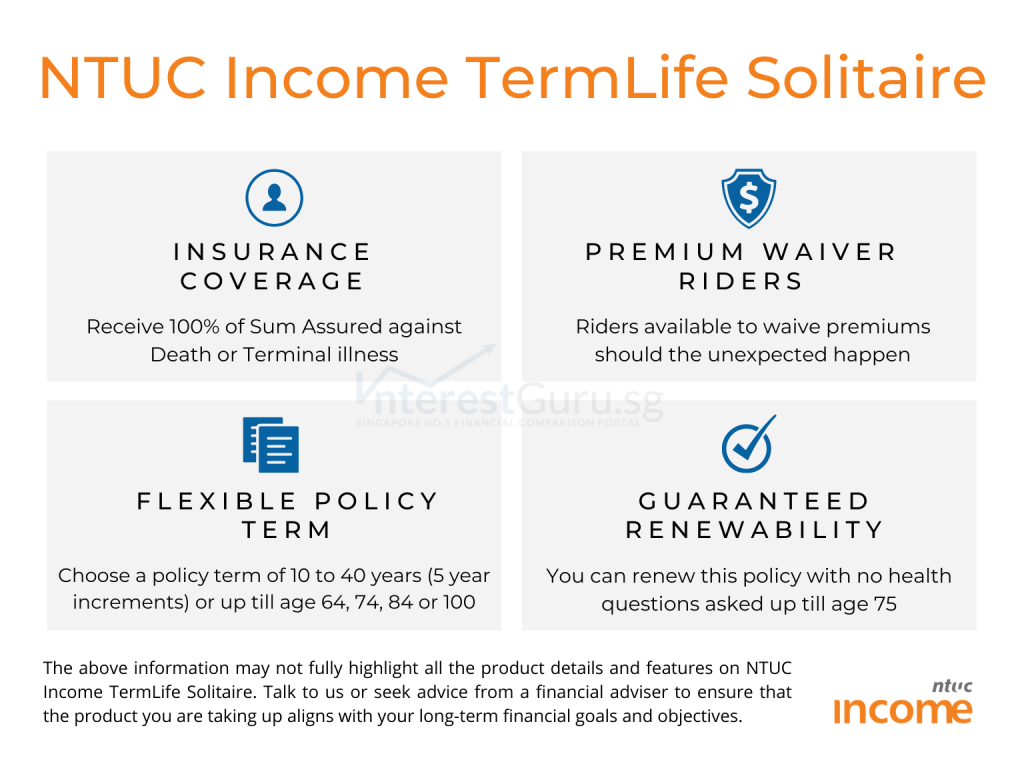

- Non-participating policy – Term policy

- Protect your financial legacy with $1 million coverage or more

- Pays the sum assured in the event of death or terminal illness

- Wide range of riders to cover you against the unexpected

- Enjoy the option of extending your coverage after your policy term expires. Guaranteed renewal of your policy up to the age of 75

NTUC Income Term Life Solitaire is a common search alternative for NTUC Income TermLife Solitaire.

Read about: Term Policy: How does it work?

Read about: 3 things to consider before taking up a new financial product

Features of NTUC Income TermLife Solitaire at a glance

Cash and Cash Withdrawal Benefits

Cash value: No

Cash withdrawal benefits: No

Health and Insurance Coverage

- Death: Yes

- Total Permanent Disability: Yes, with attached rider

- Terminal Illness: Yes

- Critical Illness: Yes, with attached rider

- Early Critical Illness: Yes, with attached rider

Health and Insurance Coverage Multiplier

- Death: No

- Total Permanent Disability: No

- Terminal Illness: No

- Critical Illness: No

- Early Critical Illness: No

Optional Add-on Riders

Disability Accelerator

Dread Disease Accelerator

Payor Premium Waiver

Dread Disease Premium Waiver

Enhanced Payor Premium Waiver

Additional Features and Benefits

Yes.

For further information and details, refer to NTUC Income website. Alternatively, fill-up the form below and let us advise accordingly.

Read about: No budget for financial planning?

Read about: How much life insurance coverage do you need?

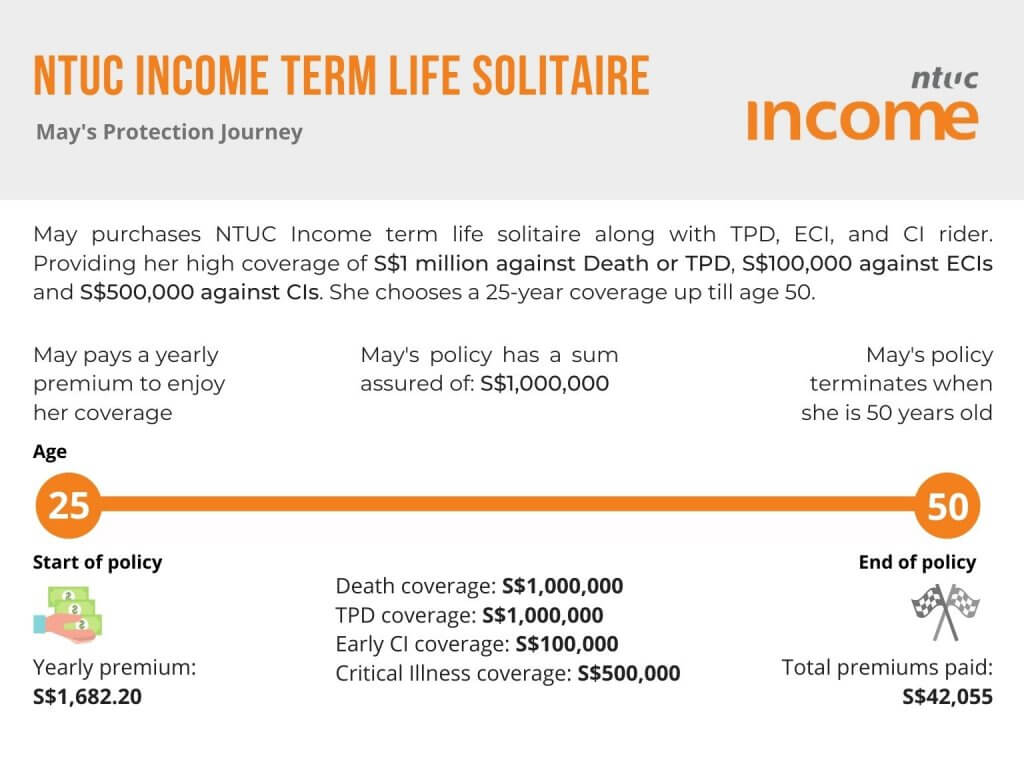

Policy Illustration for NTUC Income TermLife Solitaire, May

May, age 25, purchases NTUC Income TermLife Solitaire with Total and Permanent Disability (TPD), Early Critical Illness (ECI), and Critical Illness (CI) riders to enjoy extensive coverage.

May chooses to be covered for 25 years until age 50. He is covered with S$1,000,000 against Death and TPD, S$100,000 against ECIs, and S$500,000 against CIs.

May’s NTUC Income TermLife Solitaire policy terminates when he reaches age 50 with no cash value.

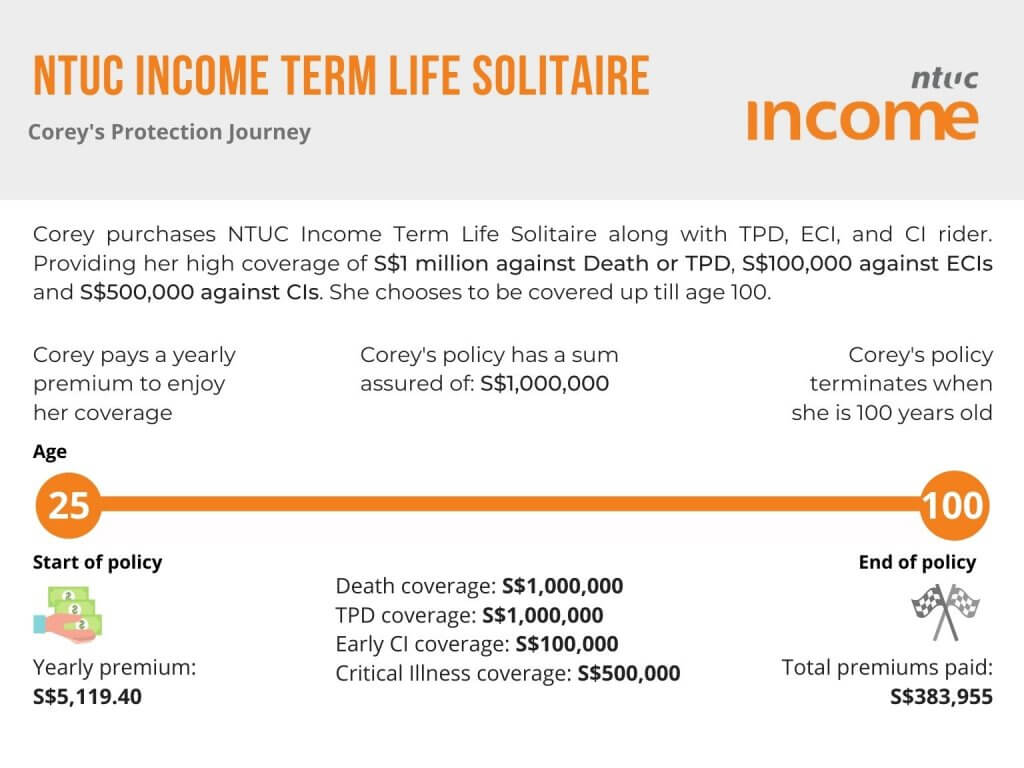

Policy Illustration for NTUC Income TermLife Solitaire, Corey

Corey, age 25, purchases NTUC Income TermLife Solitaire with Total and Permanent Disability (TPD), Early Critical Illness (ECI), and Critical Illness (CI) riders to enjoy extensive coverage.

Corey chooses to be covered until age 100. He is covered with S$1,000,000 against Death and TPD, S$100,000 against ECIs, and S$500,000 against CIs.

Corey’s NTUC Income TermLife Solitaire policy terminates when he reaches age 100 with no cash value.

NTUC Income TermLife Solitaire may be suitable if you are looking for

NTUC Income TermLife Solitaire may potentially be a good fit if the following matters to you:

- High Health and Protection coverage

- High insurance coverage for Death or Terminal Illness

- High insurance coverage for Early Critical Illness, Critical Illness or Total Permanent Disability

- Lower initial premium compared to other types of insurance policies

- Looking to boost insurance coverage or fill a shortfall in an insurance portfolio

NTUC Income TermLife Solitaire may not be suitable if the following matters to you:

- Long-term cash accumulation

- Regular cash payout

- A one-time premium commitment with no further cash commitment

- Insurance policy with a surrender value.

Further considerations on NTUC Income TermLife Solitaire

- How is NTUC Income or NTUC Income NTUC Income TermLife Solitaire and claims based on past track record?

- How does NTUC Income TermLife Solitaire compare with Term policies from other insurance companies?

- Can NTUC Income TermLife Solitaire fulfill my financial, insurance, health, and protection needs?

Read about: 8 Best Whole Life Insurance Plans in Singapore for Coverage and Wealth Accumulation (2023 Edition)

Read about: 8 Best Term Life Insurance Plans in Singapore for Coverage (2023 Edition)

The above information may not fully highlight all the product details and features on NTUC Income TermLife Solitaire. Talk to us or seek advice from a financial adviser before making any decision about NTUC Income TermLife Solitaire.

Always ensure your long-term financial goals and objectives are aligned with the financial product you are considering to take up.

Is NTUC Income TermLife Solitaire suitable for me?

Contact InterestGuru using the form below. Our panel of licensed financial advisers will advise accordingly, based on your financial profile and protection needs.

All financial reviews and proposals provided are 100% free of charge. There will be no obligation to take up any proposed financial products or services in any way.

We compare quotations head to head on all leading insurers in Singapore