4 Best Savings Endowment Plans in Singapore for Wealth Accumulation (2023 Edition)

We look for the best saving endowment plans in Singapore that provides a high guaranteed and projected cash value upon maturity.

Best Savings Endowment Plans Table of Contents

- 1 What makes a good savings plan and endowment policy

- 2 Best endowment savings plan for highest guaranteed returns – Singlife Choice Saver

- 3 Best endowment savings plan for cashback features – Manulife ReadyBuilder II

- 4 Best endowment savings plan for flexibility – Manulife Spring II

- 5 Best endowment savings plan for accidental death coverage – NTUC Income Gro Secure Saver

- 6 What can I do next?

- 7 Which Endowment Savings Plans are the most suitable for you?

Taking up a Savings plan and Endowment policy a.k.a. endowment/savings insurance usually requires a financial commitment, and the policy is meant for cash accumulation returns. The policy may or may not have withdrawal options in the later life stages of your life.

However, not all insurance policies are created equal. InterestGuru.sg looks into the 4 best Savings plans and Endowment policies that provide the most value for your money.

In this review, we take an in-depth look into the following 4 endowment savings plans that provide a high guaranteed and projected cash value upon maturity.

- Best endowment savings plans for cashback features – Manulife ReadyBuilder II

- Best endowment savings plans for highest guaranteed returns – Singlife Choice Saver

- Best endowment savings plans for flexibility (premium term) – Manulife Spring II

- Best endowment savings plans for accidental death coverage – NTUC Income Gro Secure Saver

This list of the 4 best endowment savings plans is updated as at 11/07/2023

Related article: 3 Best Savings Endowment Plans in Singapore with Lifetime Wealth Accumulation (2023 Edition) *NEW*

What makes a good savings plan and endowment policy?

We look into Savings plans and Endowment policies that provide a good blend of product features, potential payout and flexibility of saving period. While all savings plans and endowment policies accumulate cash values, the cost of insurance riders may affect your surrender value when you need a payout.

Our criteria for picking the Endowment Policies below:

- Options for cash withdrawal

- Type of payout (Guaranteed and Non-Guaranteed)

- Available riders to complement insurance coverage

- Other unique product features

Note: The Savings plans and Endowment policies listed below are not ranked in any priority. Early surrendering or cashing out from your endowment insurance policies will result in financial loss.

Read about: How does Savings Plans and Endowment Policies work?

Read about: Savings Plans and Endowment policies, are they suitable for me?

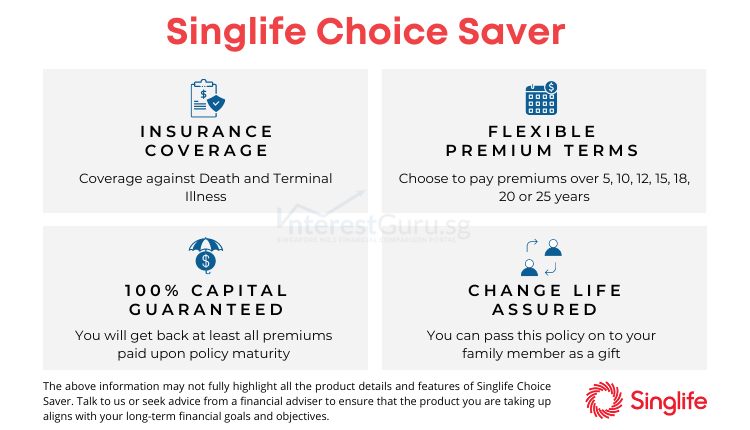

Best endowment savings plan for Highest Guaranteed Returns – Singlife Choice Saver

Singlife Choice Saver (previously known as Aviva MyChoiceSaver) is an endowment savings plan that allows you to save over a short time or for a lifetime.

Flexible premium payment terms ranging from 5, 10, 12, 15, 18, 20 or 25 years for a policy term of 10 to 25 years or up till age 99.

There is no flexibility to withdraw the funds, however, you can choose to reassign the policy to a loved one for them to enjoy the benefit of the policy. This option can be exercised twice in the entire lifetime of the policy.

Pros of Singlife Choice Saver

- 100% capital guaranteed upon policy maturity

- Option to change the life assured to your loved one to carry on the policy

- Receive an additional 3% of the sum assured upon reaching certain life milestones (i.e. marriage, buying a property, etc.) up to 2 claims

Cons of Singlife Choice Saver

- No single premium option

- Surrendering the policy any time before the policy maturity may incur financial loss

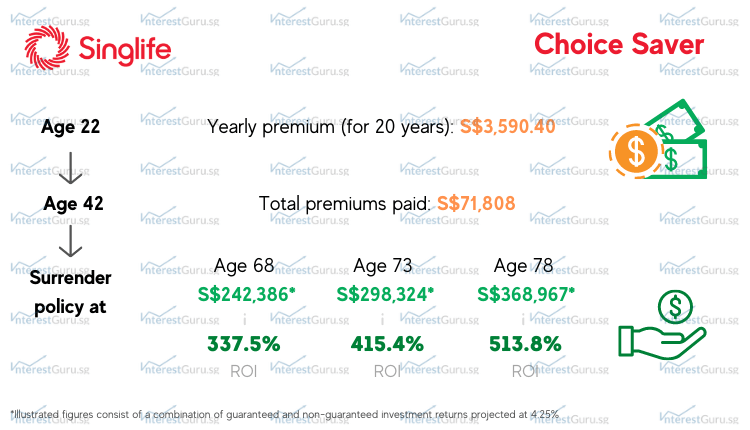

Policy Illustration for Singlife Choice Saver

At age 22, Peter purchased Singlife Choice Saver to save for his future. He pays a yearly premium of S$3,590.40 for the next 20 years for a policy term till age 99.

At age 42, Peter finishes premium payment with a total of S$71,808 paid. Singlife Choice Saver will continue accumulating cash value until Peter is age 99.

Peter has the option to change the life assured to his family member as a gift if he so chooses.

As and when Peter chooses to surrender his policy, he would receive the following:

- Age 68 – S$242,486 – 337.5% ROI (Return on Investment)

- Age 73 – S$298,324 – 415.4% ROI

- Age 78 – S$368,967 – 513.8% ROI

- Age 99 – S$951,646 (The new life assured can receive this amount at policy maturity if you do not live till age 99)

Read about: Singlife Choice Saver Review (in-depth plan details)

Alternative to Singlife Choice Saver – Prudential PRUWealth II

Prudential PRUWealth II is a whole life savings plan that allows for the option to pay a single premium with capital guaranteed from the 10th year onwards.

Pros of Prudential PRUWealth II

- Single premium option available

- Capital guaranteed after the 10th policy year

Flexible regular premium terms of 5, 10, or 20 years

- For 5, 10, and 20-year premium options, capital is only guaranteed after the 15th, 18th, and 20th year respectively

Cons of Prudential PRUWealth II

- Surrendering the policy before the capital guaranteed period could incur financial loss

Read about: Prudential PRUWealth II Review

Singlife Choice Saver vs Prudential PRUWealth II

We’ve created an apple to apple comparison between Singlife Choice Saver and PRUWealth II to find out which is the better whole life savings plan.

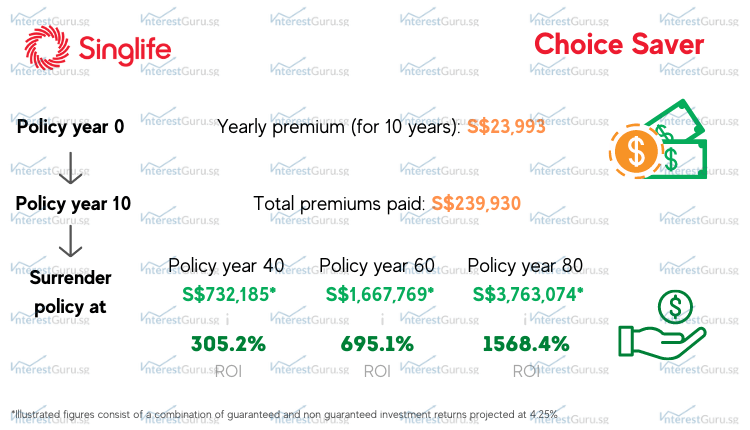

The below policy illustrations are based on Mary, a mother who purchased a whole life savings plan for her son Jason when he was just 5 years old.

Ainglife Choice Saver Illustration Comparison Table

Mary purchased Singlife Choice Saver for her 5-year-old son Jason. She pays a yearly premium of S$23,993 for the next 10 years.

When Jason turns 15 years old, Mary finishes premium payment with a total of S$239,930 paid in premiums, now policy year 10.

When Jason reaches 18 years old, Mary hands the policy over to him, now policy year 13.

Should Jason choose to surrender the policy he will receive these projected returns at:

- Age 45 / policy year 40 – S$732,185 / 305.2% ROI

- Age 65 / policy year 60 – S$1,667,769 / 695.1% ROI

- Age 85/ policy year 80 – S$3,763,074 / 1568.4% ROI

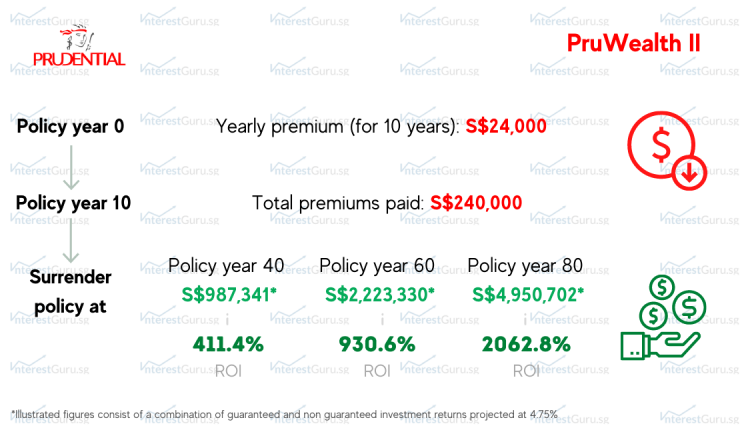

Prudential PRUWealth II Comparison Table

In another dimension, Mary purchased Prudential PRUWealth II for her 5-year-old son Jason. She pays a yearly premium of S$24,000 for the next 10 years to plan for his future.

By the 10th policy year – when Jason is 15 years old, the premium term comes to an end with Mary paying a total premium of S$240,000.

By the 13th policy year – when Jason is 18 years old, Mary hands the policy over to him.

Should Jason choose to surrender his Prudential PRUWealth II whole life savings plan, he will receive a projected:

- Age 45 / policy year 40 – S$987,341 / 411.4% ROI

- Age 65 / policy year 60 – S$2,223,330 / 930.6% ROI

- Age 85/ policy year 80 – S$4,950,702 / 2062.8% ROI

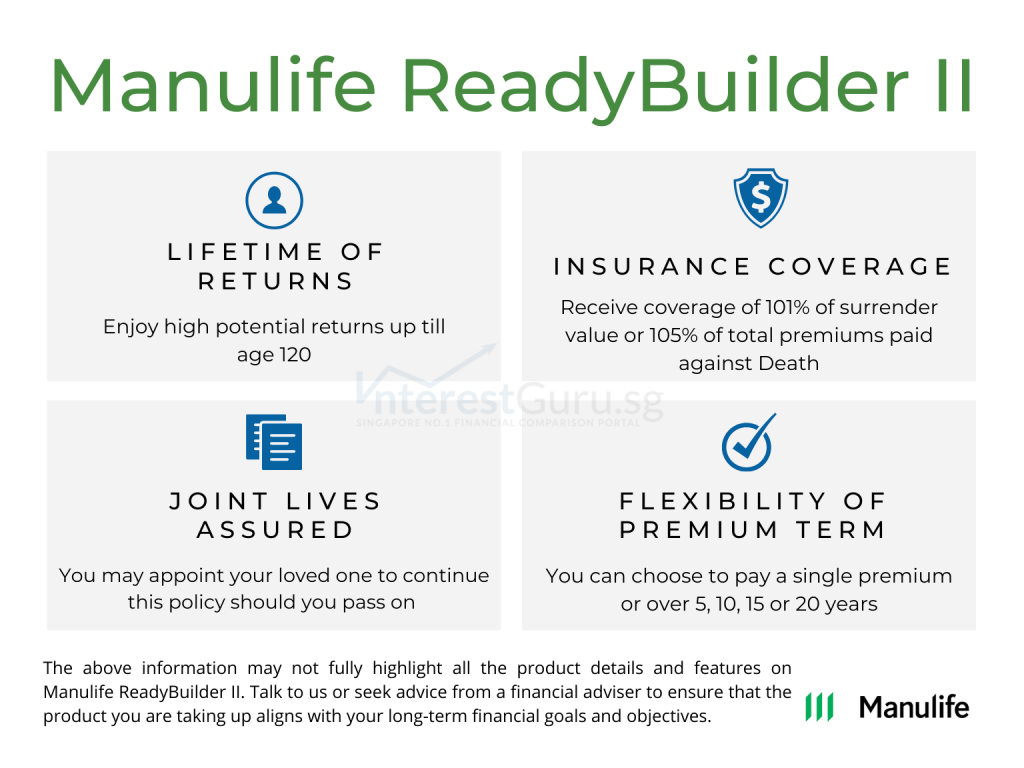

Best endowment savings plan for cashback features – Manulife ReadyBuilder II

Enjoy the freedom of unlimited withdrawals as well as lifelong wealth accumulation. Manulife ReadyBuilder II lets you achieve multiple goals in a single savings insurance plan.

Besides lifelong wealth accumulation, the policy can be assigned a loved one as the secondary life assured to carry on wealth accumulation for maximum returns, even after you have passed on.

Pros of Manulife ReadyBuilder II

- The flexibility of withdrawal from the cash value at any point in time

- The option to stop paying the insurance premium for up to a year, no penalties or interests on the payable premiums

- Continuity of plan to the next generation or third party without starting all over again from the beginning

- Wavier of future premiums in the event of Total and Permanent Disability

- Lump-sum 50% of your annual premium will be paid out if you become retrenched for more than 30 days or more

Cons of Manulife ReadyBuilder II

- Surrendering the policy any time before the 15th year may put you on a financial loss

Best endowment savings plans for flexibility – Manulife Spring II

Manulife Spring II is a 12-year endowment plan that offers 2 premium payment choices of 3 or 6 years. Depending on your choice, you will receive Guaranteed Cash Benefits from the following year till the 12th year.

You can choose to spend these payouts as you wish or accumulate them for higher returns.

Pros of Manulife Spring II

- Short premium payment terms of 3 or 6 years

- Flexible policy terms of 12 years

- Receive yearly payouts at the end of the premium term to spend as you wish or reinvest them for higher returns

Cons of Manulife Spring II

- No capital guaranteed at any point in time

Best endowment plan for accidental death coverage – NTUC Income Gro Secure Saver

NTUC Income Gro Secure Saver is a savings plan that provides you a wide range of options so you can reach your financial goals with great flexibility and ease.

You can choose to save for:

- 5 years with a policy term 10 to 25 years later

- 10 years with a policy term of 15 to 25 years later

- 15 years with a policy term of 20 to 25 years later

You will also receive an additional 100% of Sum Assured against accidental death and total and permanent disability (TPD before age 70).

Pros of NTUC Income Gro Secure Saver

- Enjoy high illustrated returns up to 4.30% p.a.

- Short premium term of 5, 10, or 15 years

- Flexible policy terms of 10 to 25 years

Cons of NTUC Income Gro Secure Saver

- No single premium payment option

- Surrendering the policy will incur financial loss

Read about: NTUC Income Gro Secure Saver Review

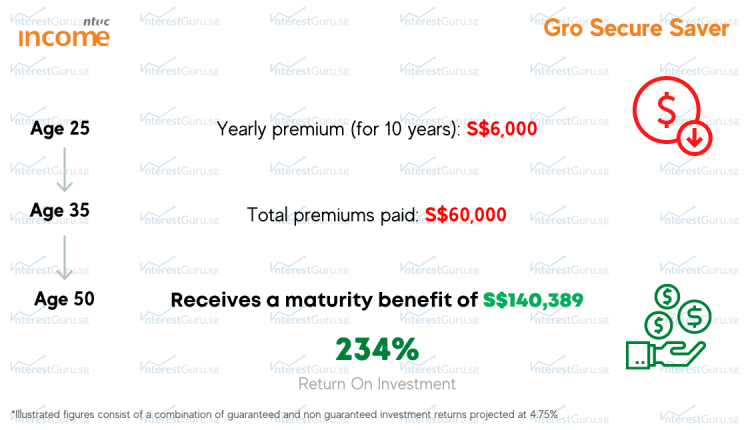

Policy Illustration for NTUC Income Gro Secure Saver

Caroline, age 25, purchases NTUC Income Gro Secure Saver to save for her future. She pays a yearly premium of $6,000 for the next 10 years.

By age 35, Caroline would’ve finished premium payment with a total of S$60,000 paid.

At age 50, Carine will receive a total projected payout of S$140,389 upon policy maturity to spend as she wish.

Alternative to NTUC Income Gro Secure Saver – Prudential PRUActive Saver II

Prudential PRUActive Saver II gives you the freedom to save a single premium or over 5 to 30 years. Your capital is guaranteed upon policy maturity.

Pros of Prudential PRUActive Saver II

- Single premium option available

- Regular premium option of 5 to 30 years available

Cons of Prudential PRUActive Saver II

- Surrendering your policy before the maturity date may incur financial loss

- You have to wait till policy maturity to access your savings

Read about: Prudential PRUActive Saver II Review

NTUC Income Gro Secure Saver VS. Prudential PRUActive Saver II

Let’s take a look at how NTUC Income Gro Secure Saver fair against Prudential PRUActive Saver II. The following policy illustration comparisons are based on a 30-year-old male with a premium term of 10 years and a policy term of 20 years.

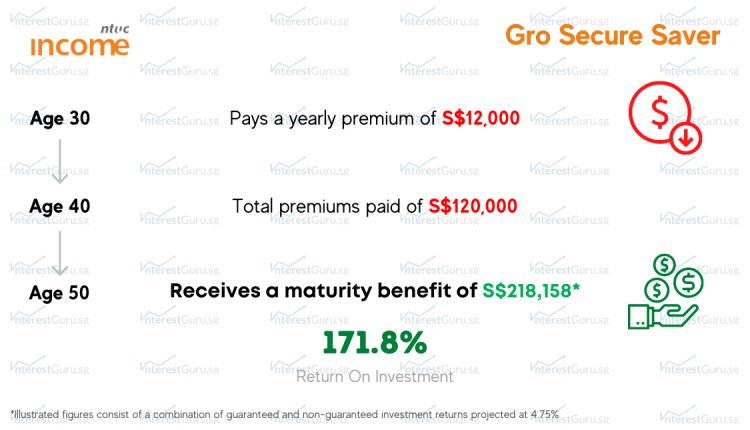

NTUC Income Gro Secure Saver Illustration Comparison Table

Max, age 30, pays a yearly premium of S$12,000 for the next 10 years for his NTUC Income Gro Secure Saver endowment plan.

By age 40, Max finishes premium payment with a total of S$120,000 paid in premiums.

Upon policy maturity at age 50, Max will receive a total of S$218,158 in total projected maturity benefit.

All in all, Max paid S$120,000 and got back S$218,158, giving him a 171.8% return on investment.

Prudential PRUActive Saver II Illustration Comparison Table

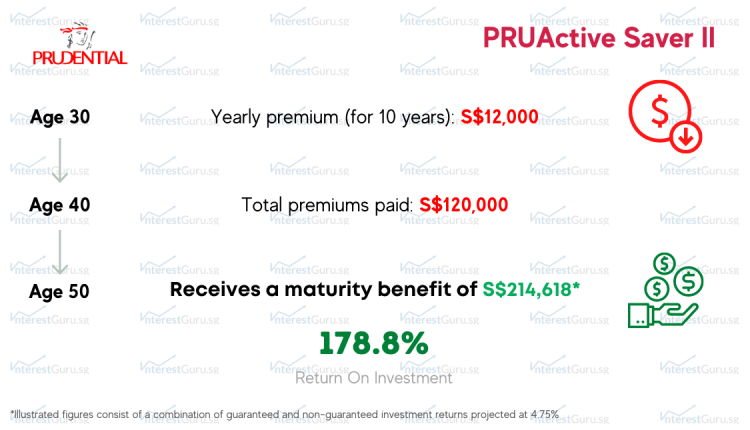

If Max had instead chosen Prudential PRUActive Saver II to save for his future, he would’ve paid S$12,000 in yearly premiums for the next 10 years.

By age 40, Max would’ve paid a total of S$120,000 in premiums.

At age 50, Max would’ve received S$214,618 in projected maturity benefit, giving him a 178.8% return on investment.

| High-income payout retirement plans for: Male, Age 45, Retire at Age 65 |

||

| Policy Details |  NTUC Income Gro Secure Saver (Payout for 20 years) |  Prudential PRUActive Saver II (Payout for 20 years) |

| Annual Premium | $12,000 | $12,000 |

| Total Premium Total premium paid for the policy: | $120,000 | $120,000 |

| Premium Term You have to pay premium for: | 10 years | 10 years |

| Policy Term Your policy matures in: | 20 years | 20 years |

| Guarantee Maturity Value Ratio vs total premium paid: | $138,120 115% | $131,119 109% |

| Projected maturity value @ 3.25% Ratio vs total premium paid: | $175,671 146% | $176,103 147% |

| Projected maturity value @ 4.75% Ratio vs total premium paid: | $218,158 182% | $214,618 179% |

Additional note:

|

||

What can I do next?

Is this your first Life Insurance policy besides your Integrated Shield Plan? Find out how exactly you should start your financial planning instead. While saving plans and endowment policies offers a better rate than bank deposits, prioritize the more important financial objectives and goals instead such as your insurance coverages.

Read about: How much life insurance coverage do you need? *Popular*

As most savings plans do not require health underwriting, such policies can be taken up regardless of your health conditions. Insurance coverages, on the other hand, require you to have a clean bill of health or you may face exclusions or rejection of your application.

Hence, it is important to ensure your health and protection coverage is already taken care of by a Whole Life, Investment Linked Policy, or Term insurance.

Read about: 3 Best Whole Life Insurance Plans in Singapore for Insurance Coverages (2023 Edition)

Read about: 3 Best Investment Linked Policies in Singapore for Wealth Accumulation (2023 Edition)

Aim to maximise the financial returns on your savings

Wherever possible, make sure that your financial budget is sufficient to cater to the payment of the savings plan, instead of overstretching and relying on any available cashback options.

We strongly recommend you to read the following articles for wealth accumulation purposes. Understand why a shorter insurance premium payment period affects your financial returns more than you would have expected.

Read about: How can I accumulate a million dollar (Realistically)

Read about: The 7 Best Regular Insurance Savings Plans in Singapore by Product Features (2023 Edition) *NEW*

Which Endowment Savings Plans are the most suitable for you?

Our partnered financial planners will draft their proposals based on your given input. Your information and details will only be used for communication with you.

All comparisons done are 100% free and solely based on your individual needs.

*For a limited time, get attractive incentives when you take up any products that is proposed by our team of financial planners.

Compare savings plans quotations from all leading insurers in Singapore

Too much work to fill in the form above?

Drop us your contact details and let InterestGuru.sg contact you instead. We will assign a licensed financial adviser to work on your inquiry at no cost to you.

Alternatively, use our CompareNOW to compare savings plans and endowment policies across insurance companies. Compare and get the best for yourself, it doesn’t have to cost you!

Best Insurance Plans in Singapore

Note: All financial figures are based on close approximate and all non-guaranteed figures are based on the higher tier of 4.75% investment returns. The sample illustrations are for illustrative purposes only and is not a contract of insurance. Early surrendering or cashing out from Endowment Savings insurance policies will certainly result in financial loss. In the event of doubt, always refer to the precise terms and conditions as specified in your policy contract. Seek the advice of a qualified financial professional or a licensed financial adviser before making any decision or financial commitment.

*Terms and conditions may apply, speak to our financial planners or drop us a message for more details.