The 5 Best Insurance Plans in Singapore for Retirement Income (2023 Edition)

Comprehensive review of the best insurance plans in Singapore that provides a stream retirement income.

You would need to draw upon your savings to fund your ideal retirement needs and lifestyle expenses. But do you have sufficient savings or regular retirement income, by the time you quit your full-time job?

Compared to other Singaporeans, where do you fare on planning for your retirement income?

A recent Nielsen survey commissioned by NTUC Income (published on 27 Aug 2018), shows that 67% of parents expect themselves to outlive their savings.

Key findings from the survey involving 400 parents (age 30-55) and 200 youth (19-25):

- A high shortfall on actual savings ($1,146/ monthly) against perceived retirement needs ($3,314/ monthly)

- Only 6% are confident of maintaining their current lifestyle during retirement, despite over 80% polled having started saving or planning for retirement.

- Average retirement planning only starts at age 36, despite the average ideal retirement age at 63

Another retirement survey by international research firm Economist Intelligence Unit (EIU) and insurer Prudential (released on 25 Sept 2018), shows the dependency on salaries for expenses and lifestyle needs during retirement:

- Among the polled 1,214 Singapore residents, only 15% expects not to rely on their salaries at all, when they turn 62.

How do you wish to receive your retirement income?

With the right insurance plans, the effects of compounding returns on your savings can allow you to build up a sizeable stream of retirement income for your golden years.

Given a choice, how would you like to receive your retirement income to fund your retirement need and lifestyle expenses:

- A high monthly retirement income, during the initial years of your retirement?

- An inflation-adjusted retirement income, ensuring your purchasing power as you age?

- A single lump sum retirement payout, anytime upon the complete withdrawal of your funds?

- A yearly retirement income, with the option to withdraw your principal savings?

- A retirement income multiplier (2x), in the event of disability during your retirement years?

Which insurance products or retirement plans will provide the best way for you to achieve the type of retirement income you desire from above?

The 5 Best Insurance Plans in Singapore for Retirement Income

InterestGuru.sg provides a list of the 5 best insurance plans in Singapore that provides a stream of income payout, based on how you would like to receive your retirement income.

This list of the best insurance plans for retirement income is not ranked in any order of preferences or priorities:

- Best Insurance Plan for High Retirement Income (20 years): Aviva MyRetirementChoice II

- Best Insurance Plan for Inflation-proofed Retirement Income (20 years): GE Supreme Retirement

- Best Insurance Plan for Lump Sum Retirement Payout: Manulife ReadyBuilder

- Best Insurance Plan for Flexibility of Capital: Aviva MyLifeIncome II

- Best Insurance Plan for Additional Retirement Income (2x due to disability): NTUC Income Gro Retire Ease

Please be aware that the above insurance plans can be further customised to provide an even higher retirement income for you.

Speak to us about your personalised illustrations, to ensure that the intended plans best reflects your retirement planning needs.

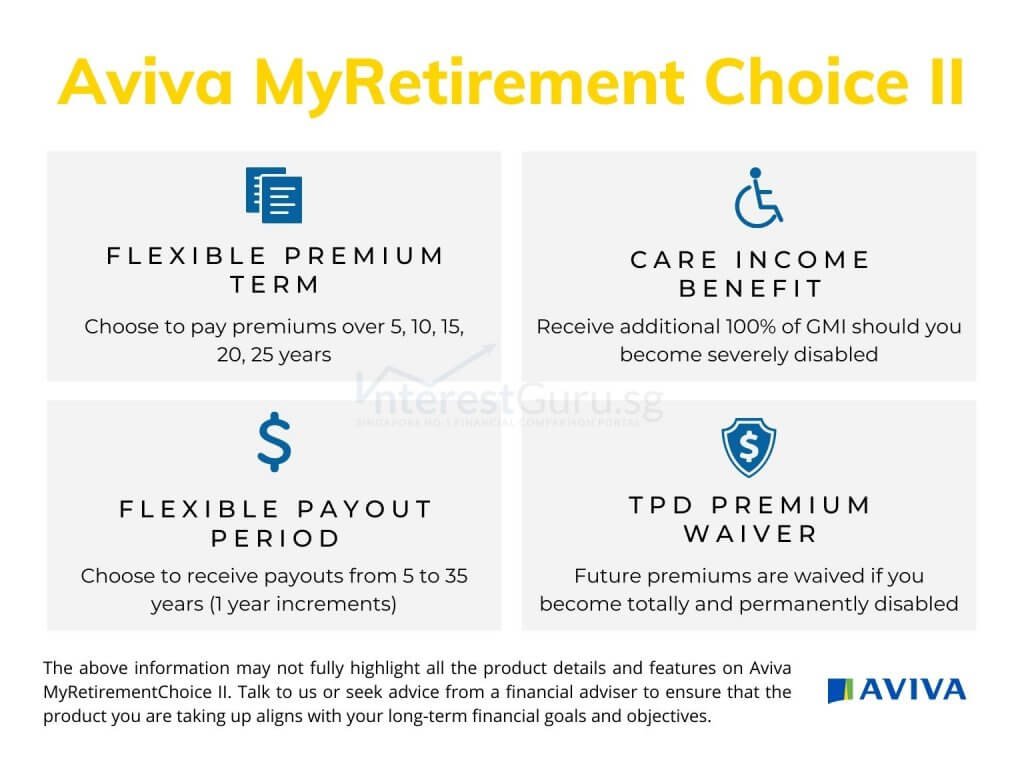

Best Insurance Plan for High Retirement Income (20 years): Aviva MyRetirementChoice II

Aviva MyRetirementChoice II is a highly competitive retirement income plan, due to the high guaranteed and projected retirement income payout.

In the unfortunate event of severe disability (failing 3 of 6 ADLs or LOI), your guaranteed monthly retirement income will be doubled.

MyRetirementChoice II also allows you the flexibility of selecting your desired retirement income options for:

- The number of years to save for your retirement plan

- The number of years to get a retirement income payout

- The preferred retirement age to start collecting a retirement income payout

Sample financial illustration for Aviva MyRetirementChoice II

Sue (female, age 40) wishes to pay the premiums on her insurance retirement plan for only 10 years. At the same time, she wants to receive a retirement income payout for 20 years starting at age 65.

With a $20,000 yearly premium, the total premium Sue paid for Aviva MyRetirementChoice II will be $200,000.

Sue can expect to receive the following retirement income:

- Total Guaranteed Retirement Income to age 85: $434,400 ($1,810/mthly x 12 x 20 years)

- Total Projected Retirement Income to age 85: $736,800 ($3,070/mthly x 12 x 20 years)

Should severe disability occurs, Sue guaranteed monthly retirement income will be doubled.

Refer to: Aviva MyRetirementChoice II review

Aviva MyRetirementChoice II is also featured in our: The 3 Best Highest Income Payout Retirement Plans in Singapore (2023 Edition)

Best Insurance Plan for Inflation-proofed Retirement Income (20 years): Great Eastern Supreme Retirement

Great Eastern Supreme retirement rewards you for reaching your desired retirement age with a lump sum payout of 24 months of your Guaranteed Monthly Income.

To ensure that your retirement income is not eroded by inflation, your guaranteed payout is adjusted upwards by 25% at the end of every 5 years of income payout.

Sample financial illustration for Great Eastern Supreme retirement

Gary (male, age 40) wishes to pay the premiums on his insurance retirement plan for only 10 years. At the same time, he wants to receive a retirement income payout for 20 years starting at age 65.

With a $19,992 yearly premium, the total premium Gary paid for Great Eastern Supreme retirement will be $199,920.

Gary can expect to receive the following retirement income:

- Total Guaranteed Retirement Income to age 85: $371,700 (Including lump sum bonus)

- Total Projected Retirement Income to age 85: $683,550

The guaranteed income that Gary receive will be adjusted to increase by 25% every 5 years. Furthermore, with a lump sum payout of $25,200, Gary can kick-start his retirement with a celebration.

Refer to: Great Eastern Supreme Retirement review

Great Eastern Supreme retirement is also featured in our: The 3 Best Inflation-proofed Retirement Plans in Singapore (2023 Edition)

Best Insurance Plan for Lump Sum Retirement Payout: Manulife ReadyBuilder

Manulife ReadyBuilder is a whole of life insurance savings plans that allow you to have a lifetime of wealth accumulation on your savings. At the same time, you can also make an unlimited number of withdrawals from the cash value within the plan.

With the option to appoint a secondary life insured, your spouse or child can continue the policy for their future wealth accumulation. At the same time, no further insurance premium is required from them as you have finished paying the premiums for the policy.

Sample financial illustration for Manulife ReadyBuilder

Joe (male, age 35) wishes to pay the premiums on his insurance retirement plan for only 15 years. He wants the flexibility to make withdrawals at any point in time from the cash value of the policy.

With a $15,000 yearly premium, the total insurance premium Gary paid for Manulife ReadyBuilder will be $225,000.

Assuming no withdrawal was done on his Manulife ReadyBuilder, Joe can fully surrender the plan and expect to receive:

- Projected surrender value at age 65: $677,270

- Projected surrender value at age 75: $997,400

Joe can also choose to make a partial lump sum withdrawal from the plan for his retirement income and let his loved ones retain the policy for continual wealth accumulation.

Refer to: Manulife ReadyBuilder review

Manulife ReadyBuilder is also featured in our: The 7 Best Regular Insurance Savings Plans in Singapore (2023 Edition)

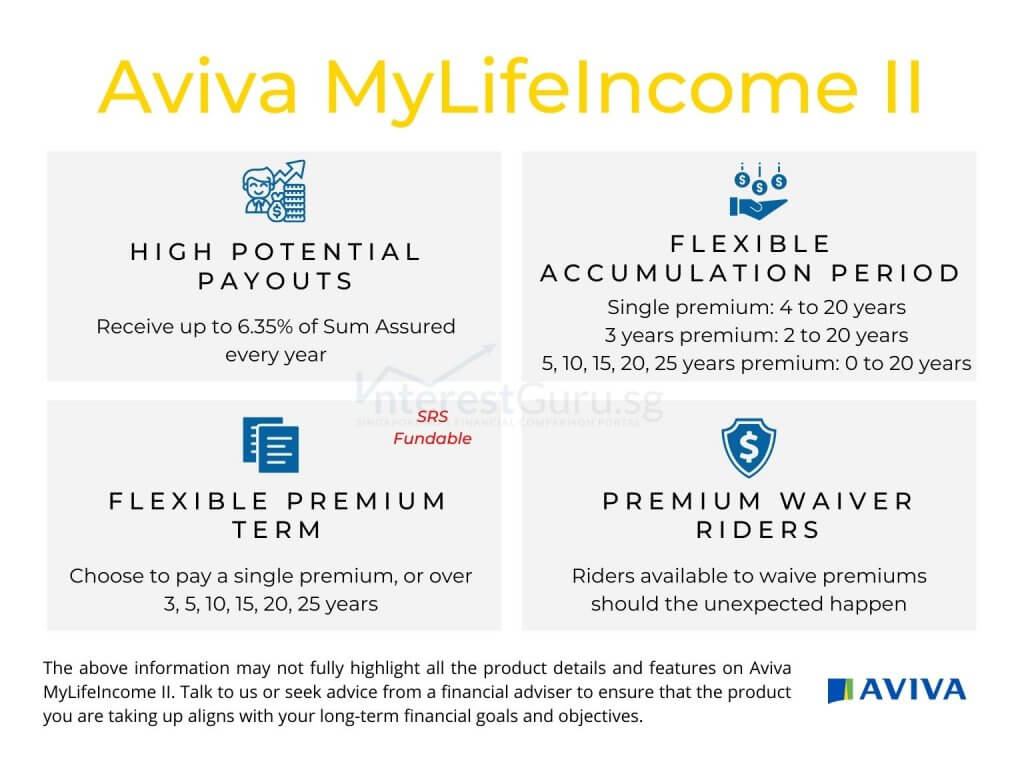

Best Insurance Plan for Flexibility of Capital: Aviva MyLifeIncome

Worried about missing out on other opportunities with your savings locked up in an insurance retirement plan? Or somehow you got tired of a monthly payout from your annuity plan?

Aviva MyLifeIncome can be surrendered and you are guaranteed to get back all the premiums you paid for this retirement income plan.

With Aviva MyLifeIncome, you will get a lifetime of retirement income as hold as you hold on to the insurance plan. At the same time, you can surrender the plan for a lump sum payout of all the premiums paid.

What’s more, the guaranteed lump sum payout upon the surrendering of MyLifeIncome is independent of all the income you have received till then.

For the most demanding yield hunter, your retirement income payout can start as soon as 4 years after placing a single lump sum for this income plan.

Sample financial illustration for Aviva MyLifeIncome

June (female, age 45) wishes to pay only a single lump sum for her insurance retirement plan. She chooses to receive a retirement income payout right at the end of the 10th policy year (age 56).

With a single premium of $250,000, June is guaranteed to receive a minimum sum of $250,000 if she chooses to surrender the Aviva MyLifeIncome for the policy cash value anytime after age 53.

As long as June hold on to her Aviva MyLifeIncome, she can expect to receive:

- Projected Yearly Retirement Income from age 56: $16,400

Should June choose a later age to start collecting her retirement income, the payout will be significantly higher.

Refer to: Aviva MyLifeIncome review

Aviva MyLifeIncome is also featured in our: The 3 Best Retirement Plans with Guaranteed Principal Withdrawal in Singapore (2023 Edition)

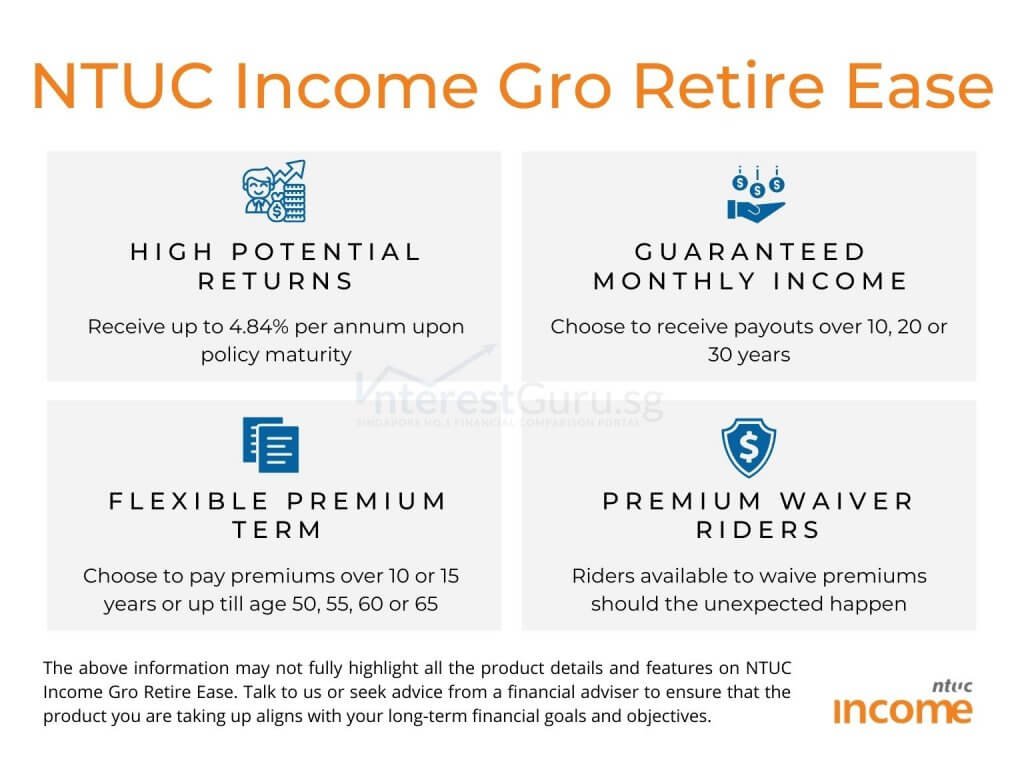

Best Insurance Plan for Additional Retirement Income (2x due to disability): NTUC Income Gro Retire Ease

NTUC Income Gro Retire Ease is one of our personal favourite for retirement income plan across all the insurance companies in Singapore. RevoRetire offers a high retirement income payout and the most competitive disability income multiplier benefits.

With all other insurance retirement plans offering multiplied income payout upon failing a minimal of 2/3 of 6 ADLs, NTUC Income Gro Retire Easecomes with an attractive Disability Care Benefit.

With old age, comes the challenges in performing your daily physical movements. However, you may not trigger an income payout multiplier from other retirement plans unless you meet the criteria of failing the ADLs.

For NTUC Income Gro Retire Ease, your guaranteed monthly retirement income is doubled with any one of the following:

- Loss of use of one limb

- Loss of speech or hearing

- Sight in one eye due to accidental injury or illness

To top it off, the monthly retirement income payout is highly competitive and worthy of being one of the best among its peers.

Sample financial illustration for NTUC Income Gro Retire Ease

Mr Lee (male, age 45) wishes to pay the premiums on his insurance retirement plan for only 5 years. He wishes to receive a retirement income payout for 20 years starting at age 65.

With a $40,000 yearly premium, the total premium Mr Lee paid for NTUC Income Gro Retire Ease will be $200,000.

Mr Lee can expect to receive the following retirement income:

- Total Guaranteed Retirement Income to age 85: $376,320 ($1,568/mthly x 12 x 20 years)

- Total Projected Retirement Income to age 85: $670,320 ($2,793/mthly x 12 x 20 years)

Should there be a valid claim on Disability Care Benefit, Mr Lee’s guaranteed monthly retirement income will be doubled.

Refer to: NTUC Income Gro Retire Ease Review

NTUC Income Gro Retire Ease is also featured in our: The 3 Best Highest Income Payout Retirement Plans in Singapore (2023 Edition)

Is it important to build a stream of retirement income for your future years?

You can compromise on your retirement by choosing to retire at a later age and minimising your lifestyle expenses. Alternatively, you can maximise your retirement savings by planning early.

For those seeking a high and stable income, investment in retirement annuity plans should be the major component of their financial portfolio.

When you chose to retire, working should be a choice and not a need.

Have no short-term plans to withdraw the savings in your SRS account? You can even use your CPF SRS savings to build up your retirement income, via an SRS-approved retirement plan.

What are the insurance plans that can generate the best retirement income stream for you?

It is important to have your retirement plans are structured according to your ideal retirement lifestyle and expenses.

Like to know the actual financial returns of specific insurance retirement plans based on your age, budget and financial profile?

Use our retirement planning selector to get INSTANT QUOTES based on your individual profile now!

Let us find the best retirement income plans for you!

Our partnered financial planners will draft their proposals based on your given input. Your information and details will only be used for communication with you.

All comparisons done are strictly confidential and solely based on your individual retirement needs.

*For a limited time, get attractive incentives when you take up any product that is proposed by our team of financial planners.

Compare retirement income plans across all leading insurers in Singapore!

Securing the best retirement income plans has never been this easy!

Drop us a message to have a retirement plan structured to your needs by a licensed financial adviser. Don’t worry, there is no obligation to take up anything and consultation is 100% free!

Note: All financial figures are based on close approximate and all non-guaranteed figures are based on the higher tier of 4.75% investment returns. The sample illustrations are for illustrative purposes only and is not a contract of insurance. Early surrendering or cashing out from Retirement plans or Annuity policies will certainly result in financial loss. In the event of doubt, always refer to the precise terms and conditions as specified in your policy contract. Seek the advice of a qualified financial professional or a licensed financial adviser before making any decision or financial commitment.

*Terms and conditions may apply, speak to our financial planners or drop us a message for more details.